Crompton Greaves gets a new lease of life

A series of restructuring measures, including sale of its loss-making overseas power unit, has helped the company clear its debt of Rs 900 cr

Hamsini Karthik | Mumbai

April 4, 2016 Last Updated at 21:22 IST

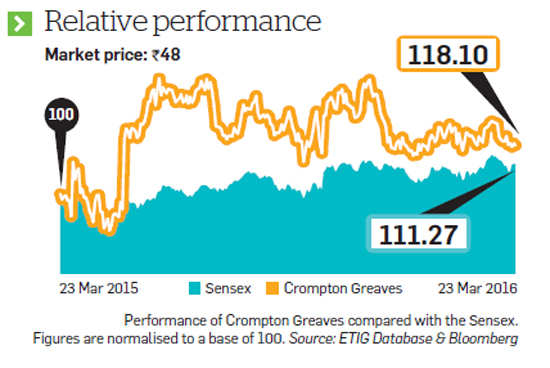

Until mid-February, the stock market did not expect any noteworthy rebound from Crompton Greaves, the company owned by debonair businessman Gautam Thapar. Then came the much-awaited news on the sale of its international power business to First Reserve International, a private equity fund, for Rs 850 crore. It boosted sentiment around its stock, which now trades at Rs 48, drawing its value from the residual power and industrials businesses (also referred to as business-to-business or B2B operations).

Crompton Greaves Executive Director (finance) Madhav Acharya says that with the sale of its international business, which clocked revenue of Rs 4,800 crore in FY15, a large part of the issues the company faced attributable to its international business and its associated debt burden is being put to rest and that the company should clock revenues of Rs 6,500 crore in 2016-17.

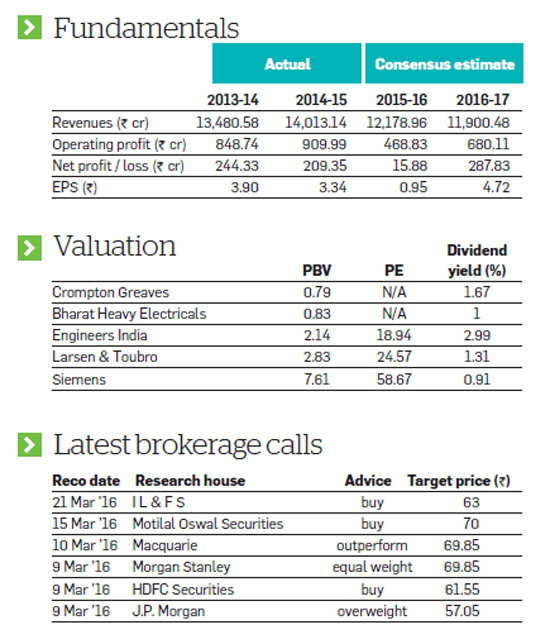

Seen against the stand-alone revenues of FY15 (excluding the consumer business), the confidence to steer a revenue growth of over 40 per cent in FY17 stems from the fact that net debt which stood at Rs 900 crore in the December quarter has more or less been repaid now, making Crompton virtually a debt-free entity. This implies an annual interest cost saving of nearly Rs 60-70 crore going forward.

Many elements have come to the rescue of Crompton. The company commenced its FY16 operation with a gross debt burden of about Rs 2,750 crore. This gradually reduced after divestment of its non-core assets and demerger of its consumer business. Among the noteworthy transactions, sale of land in Kanjurmarg (Mumbai) fetched about Rs 500 crore, while Rs 700 crore of debt was transferred to its consumer business as part of the demerger process.

Gautam Thapar Thapar sold this business to private equity funds Advent International and Temasek Holdings for Rs 2,000 crore last year. Though home-grown Havells too was in the race for the business, Thapar chose to close the deal with the funds. And finally, after months of speculation about whether the deal was still on the table, sale of its distressed international power business did the last bit of help for Crompton.

These restructuring measures may decelerate the pace of revenue growth in the near-term. The consumer business had revenue of Rs 3,200 crore in FY15. It also lent help to the company’s overall margins, given that the business generated EBIT (earnings before interest and tax) margins of 6 per cent till Q2 FY16. On the other hand, though loss-making international power business accounted for almost half of the division’s top-line, its sale will boost the company’s profit and loss statement in the next five to six months, given its track record of sequential EBIT losses posted since FY15, thanks to dismal order flows and execution hiccups in the international business.

Losing out to competition

Acharya explains that trouble in the international power business began when Crompton undertook restructuring to reduce its costs to become globally competitive. Hence, it shifted some of its projects from its manufacturing facilities at Belgium to Hungary. The delay by customers in approval and time taken in building competencies at the Hungarian facility led to increased cost of manufacturing and, in turn, led to losses.

But the good news, he points out, is that though this business is sold to First Reserve International, Crompton retains the technological expertise gained from its international plants and will use it to serve its valued clients. This puts to rest one of the primary concerns the Street had with respect to its technological capabilities, particularly in the 765 kilovolt (KV) space. Acharya affirms that the international acquisitions have helped Crompton gain technological know-how and now it is self-sufficient in this area.

Its product profile stretches up to 1,200 KV in the transformers space. With the existing capabilities, he says, the company is well prepared to take on the competition from domestic and foreign players.

Consequently, capex plans seem quite limited at the moment, except that the company plans to shift its manufacturing base closer to the Mumbai port to cater to its West Asian clients. But, this too is over a span of four to five years and may partly be funded from proceeds of the sale of its existing Kanjurmarg plant.

Going forward, given the 14-months visibility on the transformers and switchgear business with an order book of Rs 8,000 crore, Acharya is confident of an improved performance in the power division. Within the industrial segment, low traction motors is where the company is placing its bet on, given the significant improvement in demand for these products and rapid sustainable growth emanating for this business from the Indian Railways.

In wait-and-watch mode

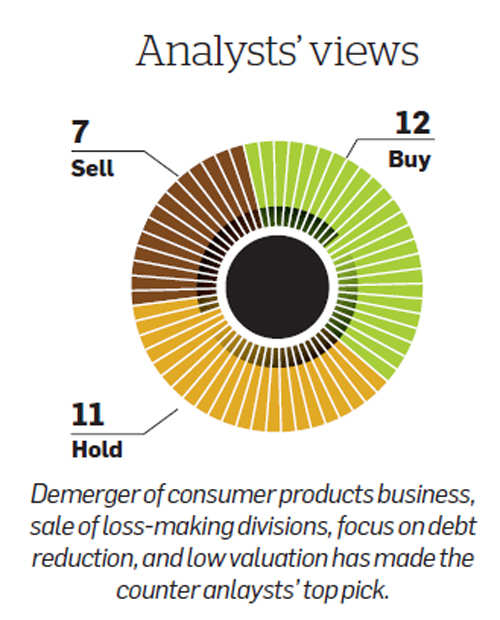

That said, though the management guides for a leaner and fitter B2B business growth in FY17, the Street prefers to watch these indicators cautiously. Analysts say that while the power business, now accounting for half of standalone revenues, is not technology-intensive, doubts persist on the scalability of its industrials segment.

Misal Singh, analyst at Religare Capital Markets who recommends ‘buy’ on the Crompton stock, points out that there are a few gaps in its switchgear business. “That apart, though Crompton has always been positioned as the third largest player in the motor business, ABB and Siemens continue to dominate the market in India,” he adds.

Renu Baid of IIFL adds: “The technology Crompton has is adequate at the moment. But if one has to maintain pricing power and stronger margin profile, it needs to move up the chain where competition is relatively less.”

According to Singh, revenue growth of 5-8 per cent is a realistic target for company. Analysts feel that it would be crucial to watch how the B2B business plays out once the sale of international power business concludes. Operating margins too, they say, may only be in the 6-8 per cent level, given the pricing pressure on the industry. Seen against the subdued Street expectation, delivering the promised goods under tough operating conditions in FY17 would be critical for Crompton to win back the investor confidence.